December 29, 2024 Investing 7 comments

On a Journey to Financial Independence: Lessons, Mistakes, and Thoughts on FIRE

I have always been fascinated with financial independence and have made financial goals for myself throughout the years. Here are some of my history with money and thoughts on FIRE.

I want to tell my own story so you don’t have to repeat my mistakes. As a disclaimer, I’m not a multi-millionaire and this is not professional financial advice. I bear no responsibility for your actions. Seek professional advice if needed (though beware that advisors have their own interests and may see you as a target to sell you something).

What’s FIRE?

FIRE stands for Financial Independence, Retire Early. Idea is fairly simple: accumulate x25 of your intended annual spending and go retire early. I wouldn’t know the origin of the term FIRE but the idea isn’t that new and I’ve always followed MMM (Mr. Money Mustache) blog which in my opinion is one of the top voices on FIRE, though with higher emphasis on frugality. I highly recommend you read some of the articles there. I will get back to FIRE after giving a brief history of my dealing with money.

Ukraine

I was raised in a working class family in Ukraine, we didn’t have money, basically we were poor. Luckily having no money didn’t stop me from getting a good education. I made my first money in a local software engineering company. At that time I’d already read some books on financial independence and wanted to invest, but tools available back then in Ukraine were limited and I mostly made guaranteed security deposits, which didn’t make too much of a difference. At very least I was smart enough to know that keeping money under the mattress was a mistake, but even banks were not reliable so I had to juggle between different banks to diversify. Most people saw value in buying real estate and who could afford would buy an apartment in the city. There was a cold awakening in 2008 when home prices dropped, yet real estate is still seen as a tangible investment you can see and touch. There is some merit to it, again will get back to it.

Austria

As I moved to Austria in 2012, I had access to more investment tools and ways of buying my first stocks. I could finally practice at least some of what I read in books on investing. Since I didn’t have much money and banks in Europe are greedy on fees, any active investing approaches were only making money for brokers. I clearly remember how I had a small amount of MSFT stock and at dividend distribution out of 14EUR I would get 0.01 after all of the fees and taxes (what a joke). For the record, those 5k in MSFT invested then would have been 46k today, but I did sell with some small profit. Lesson here is that time in the market beats timing the market. Other than spx500 and a few other stocks, at that time, I also had money invested in some mutual funds of real estate in Austria, which probably was some of my worst investments because of ridiculous management annual fees >1% and growth that didn’t even catch up with inflation (what a joke). Lessons here are to never blindly trust bank/financial advisors as they have something to sell to you and also: fees are evil. For about 4 years I was a self-employed contractor software engineer to the IAEA via another company and had a chance to understand the taxation system a bit better. I had a tax advisor, and was claiming some business expenses (like laptop, internet bill, etc) to reduce my gross income. My last year in Austria was as a staff member of the IAEA so I didn’t have to pay taxes (yes, legally) and also since I was leaving Austria I was able to withdraw all of my retirement money and I did put most of it into real estate, if invested in early 2018 into s&p 500 that would have been 2x.

Canada

Canada finally made it possible to have proper investing tooling at my disposal. Other than directly receiving AMZN/GOOG shares from my employers I invested as much as I can into low fee index tracking funds (e.g. Vanguard S&P 500, or Canada companies), of course, after maximizing my RRSP and TFSA. For US readers, RRSP is an equivalent of 401(k) plan and TFSA is a unique Canadian vehicle which is a fully tax free investment account (even on withdrawal). Being a Vancouverite, I’m obliged to bring up the topic of real estate. Vancouver is one of the most unaffordable cities in the world. I have no idea how people with regular <100k incomes can make their ends meet here. I did buy a 1.2M$ townhouse here in 2022 and I regret doing so. It may eventually prove to be a good investment if there is another crazy growth as in 2021 but so far I don’t see a way to sell the place for the price I bought it for and if I had all the money I put into it invested I would have made an extra 200k. If I had to sell it now I would lose money. Though if I was lucky to buy a place with the same money just two years earlier I could have potentially made 800k all with borrowed money. You probably know of people who preach using borrowed money to make money, like Robert Kiyosaki. I have multiple friends who rode the wave.

Now

As of 2024, I am not a multi-millionaire even though I worked for two of the FAANG companies in the past 7 years. I see this as a mistake of my own for not pushing to work for these big companies earlier in my career and not moving to the USA, even temporarily. Yes, yes, Canada pays peanuts even if you work for the big boys. Well, to be objective, compared to average Canada salaries I get paid crazy money. Yet, it often feels unfair to work on the same projects and same/similar teams as people just across the border and getting paid an entire pay grade lower. I love Canada and wish we can do better.

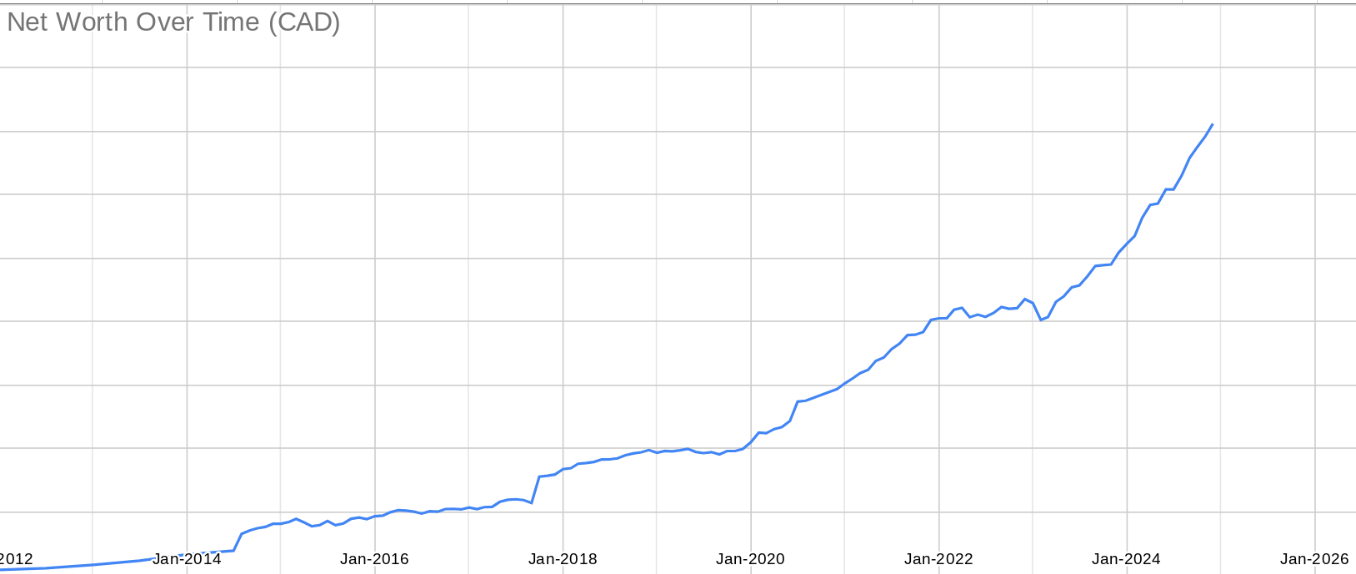

To recap the above history, here is a timeline of my net worth (sorry for no Y-axis):

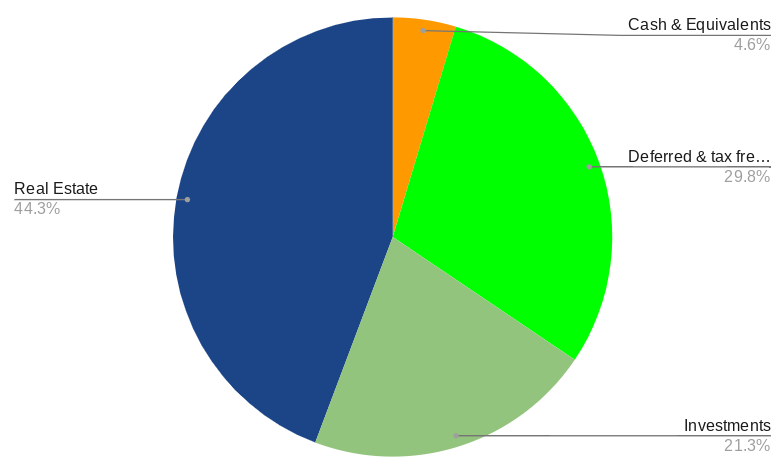

I’ve been obsessively tracking my money since 2012. Every month I would add a record to my google spreadsheet with all of my accounts, it would give me a picture of what is happening to my net worth, what’s the distribution of investments, etc. For example, this is how the overall distribution currently looks like. I’m not proud of a huge portion of real estate and even those 4.6% of cash seems a bit too excessive to my taste, so it’s something to work on.

Back to FIRE

Ask yourself a question: when you retire will you have enough money to last for as long as you need? Would you run out of money? Would you die with too much money in your bank accounts?

Personally I don’t want to die with tens of millions in my bank accounts, I would help my kids to stand on their own feet but they have to make their own money. I’m also happy to donate my money at the time of my death, but I also want to have life while I still can enjoy it. Running out of money at old age sounds like a nightmare.

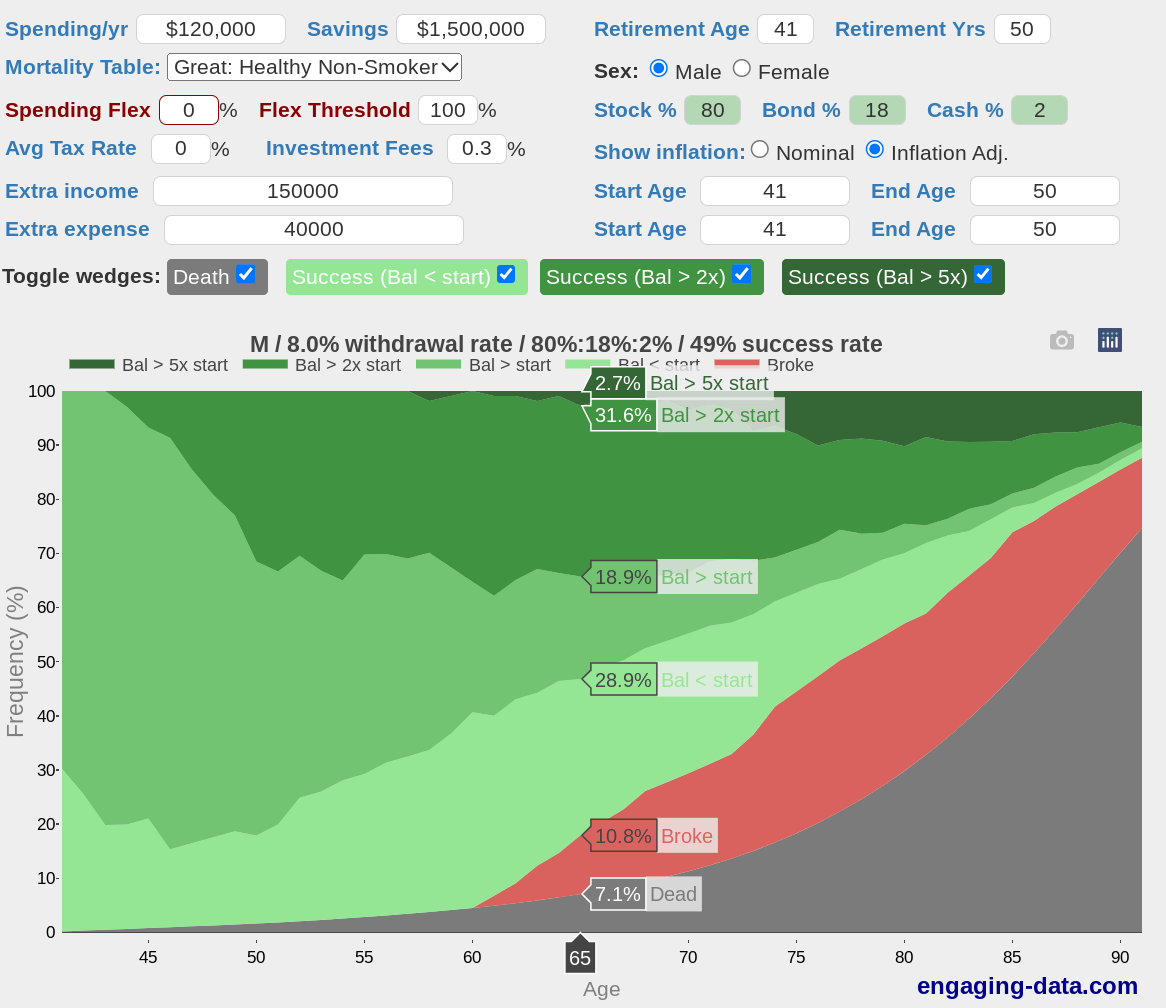

Let’s say, I want to semi-retire at age 41 with 1.5M$ in bank and then fully retire at age 50. Semi-retirement means moving to low effort gigs with ~150k income but still funding kids education 40k/y till I’m 50 years old. If I’m healthy and want to have a comfortable life with 120k/y spend, then my probability of running out of money at age 65 is 11% or being dead is 7%. Play with this Rich, Broke, or Dead calculator. It is fun:

It does seem like 1.5M$ doesn’t cut it to retire at 41 if I would want to eliminate probability of running out of money. By now, you should be asking why 41. It’s fairly simple: when I was in my early 20s I had this idea of becoming a millionaire by the age of 41 and moving to a cheaper seaside European country, like Croatia or Spain. It is now clear that 1M$ doesn’t cut it if you are raising 2 kids in North America and want to retire that early, at the very least for me.

What would be your number? The simplest way is to take your annual spending and multiply it by 25, theoretically once you reach that number you should never run out of money. Here is a more detailed calculator for your numbers: https://engaging-data.com/fire-calculator/

Conclusion

It is hard to predict the future but you can take the best educated guess, check your odds and plan for the best outcomes. I understand that for some of you talking about millions in bank accounts may sound like a lot of money and for some it may sound like peanuts (NVIDIA guys?). Do not compare yourself to others – everyone has their own path, fights their own battles and demons, you just don’t know. I’m guilty of comparing myself to others – a sure way to feel miserable. The best thing we can do is to improve our chances of winning our own battles and it’s fair to learn from others but not to envy them or to be condescending to them. If there’s one thing I hope you take away from my story, it’s to take control of your financial future.

Riding the Waves: Can We Predict the Next Big Technology Surge?

October 13, 2024 Investing No comments

“What goes up will go down” is just such a fundamental and universal concept you can apply to anything: physics, emotions, life, financials. In this post I want to have a bit of a technology view on this and also try to understand if we can ever predict and catch the “up” wave. Do you wish you had invested in NVIDIA in early 2023? I definitely wish so.

First of all let’s have a look at some of the promising technologies from the past that rode on hype and then declined in their popularity:

- Bitcoin

- UP: Do you remember all the crazy hype surrounding bitcoin and people getting rich out of nowhere? I personally have a very small amount in a Bitcoin ETF (which didn’t grow much), but know a friend who lost keys to a wallet with a dozen bitcoins, and another one who kept telling me that one bitcoin will be worth like 4 apartments in NYC.

- DOWN: Well, bitcoin as well as the blockchain technology behind it didn’t disappear, but the hype is definitely not there any longer. It is very likely we won’t see a huge rise again (or maybe we will see?). Scalability, regulatory and other reasons made this slow down. Some niche applications of blockchain are thriving though.

- Windows Phone

- UP: Ok, you might be asking “what is this?” or “why is it here?”. I included it here because I personally worked for about 1 year on a Windows Phone project back in 2011. The promise was that this will rival iPhone and Android devices.

- DOWN: the market simply did pick this one up, there wasn’t enough of app development and MS eventually pivoted to something else.

- Augmented/Virtual Reality

- UP: Another major hyped technology. Think about Google Glasses or META’s Oculus or Microsoft’s HoloLens, these technologies promised to revolutionize gaming, work, entertainment, and everyday life.

- DOWN: I didn’t buy this hype myself because it somehow makes me disgusted imagining myself living and interacting with people in a virtual world instead of the real one. Again, some niche applications still exist.

- Artificial Intelligence (AI)

- UP: So I’m sure you have read about multiple waves of AI technology, early 50s when it first appeared, 80s when expert systems were promising to change everything and (drumroll…) now when Generative AI is the next big promise.

- DOWN: I don’t know when the exact time for the downturn will come, but there are obvious problems with it (high compute costs, wrong facts, plagiarism – I make it a point not to copy anything from GenAI into my posts).

- Many other technologies of different scale (3D printing, 3D TV, BlackBerry, delivery drones, Fire Phone, etc, etc)

Potentially we can generalize abovementioned technology trends into three categories of downfall:

- Complete disappearance: VHS, CD, BlackBerry, etc.

- Reduction to niche usages: VR for gaming, 3DPrinting for specific applications, etc.

- Enduring: Personal Computers, Internet

Now, where am I going with all of this? I’m trying to ask myself a question: is it possible to guess for any new technology if it is going to disappear, get reduced to a niche use, or will endure beyond our lifetime? Additionally is it possible to catch the “up” wave and ride it until the peak?

Let’s take the case of NVIDIA. If AI is a gold rush, NVIDIA is selling shovels. I found an article from 2019 arguing that NVIDIA will supras Apple in market cap, the argument states that the AI market will grow to 15T$ and that the computer is switching to GPU which logically makes sense.

Here are some recommendations for my future self to be on the lookout:

- People have entire careers dedicated to spotting these trends so it makes sense to be aware (re-subscribed to weekly TechCrunch newsletter).

- Spot tech industry trends using professional networks.

- Spend dedicated time once monthly thinking about well positioned companies (scheduled time for myself).

- Do my own numbers once anything appears interesting (this is a difficult one, but it would set you ahead of others, think of “The Big Short” movie).

- Risk here and there.

Do you have any thoughts on the topic? What is that big thing you missed, you think you could have caught?